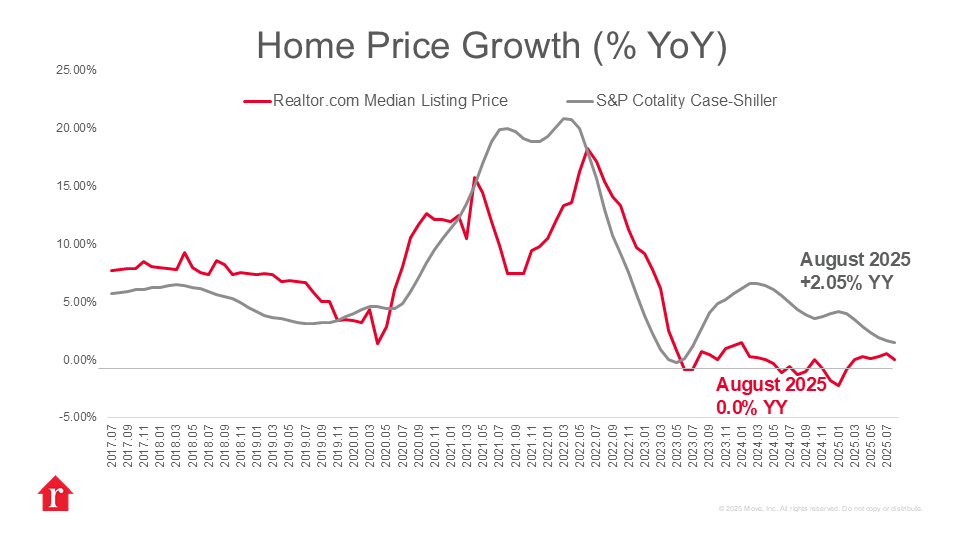

What does the data show?

The S&P Cotality Case-Shiller Index rose 1.5% annually in August, although at a slower pace as affordability constraints weigh on buyers. This month’s release reflects closings from June through August, a stretch of the summer market marked by steady mortgage rates in the mid-to-high 6% range and modest improvements in inventory. The 20‑City Composite increased 1.6% and the 10‑City Composite rose 2.1%, marking among the weakest annual gains in recent years. While borrowing costs remained elevated, they were less volatile than earlier in the year, helping to stabilize buyer sentiment. Still, many prospective buyers stayed sidelined due to high monthly payments and constrained affordability, limiting the pool of active shoppers and dampening momentum in several major markets.

How did trends vary by region?

Regionally, markets in the Northeast and Midwest continue to perform relatively better, supported by tighter resale supply and steadier demand. Cities such as New York City, Chicago and Cleveland stand out among the 20‑city composite for their above‑average price gains. By contrast, many metros in the Sun Belt and West, including Tampa, Phoenix and Las Vegas, are showing clearer signs of softening: inventory is recovering more rapidly, homes are taking longer to sell, and price cuts and delistings are bec